Global Forum For Indurstrial Devlopment is SPONSORED BY ICO INDIA

- MP Society Registration (Act. 1973 No. 44) 03/27/01/21857/19 (MSME Forum Established Since-2009)

Scripbox's proprietary algorithm selects the best funds each year based on factors like age of fund, historical growth rate, consistent performance, size of fund, top 10 holdings and more. This helps you stay invested in the best funds always, without putting in the effort to research and select funds from around 6000 options!

There is NO lock-in period for equity or debt mutual funds based plans. You can withdraw the money anytime, however Scripbox recommends a investment horizon of at least 3 years for Short Term Money & 5 years for Long Term Wealth. There is a 3 year lock-in period for ELSS funds in Scripbox Tax Saver.

Our investment dashboard provides a summary of the wealth accumulated & capital gains/loss for different plans. This helps you track the progress of investments made towards all your financial goals.

To many people, Mutual Funds can seem complicated or intimidating. We are going to try and simplify it for you at its very basic level. Essentially, the money pooled in by a large number of people (or investors) is what makes up a Mutual Fund. This fund is managed by a professional fund manager.

It is a trust that collects money from a number of investors who share a common investment objective. Then, it invests the money in equities, bonds, money market instruments and/or other securities. Each investor owns units, which represent a portion of the holdings of the fund. The income/gains generated from this collective investment is distributed proportionately amongst the investors after deducting certain expenses, by calculating a scheme’s “Net Asset Value or NAV.

Before taking any investment decisions, it is crucial to educate yourself about the different aspects of those investments. One such aspect to understand is the tax implication of your investments on your long-term and short-term capital gains. But what does capital gains mean? Read on to get a better understanding.

The annual US FED symposium conducted by the Kansas City Fed at Jackson Hole is a key event on the economic policy calendar. The current year’s symposium was keenly watched as the markets expected the FED Chair to lay out the path for “Taper” in the context of strong economic rebound and inflation above the target range. The outcome has been favourably received by the markets as the FED Chair made a clear distinction between “start of taper” and an eventual “lift off ‘’ with respect to policy rates. While based on current estimates, tapering could potentially start by the year end, the marker for eventual rate actions has been clearly set higher based on substantialfurther progress on employment along with sustainable inflation of 2% or above. Noise surrounding Delta variant could possibly push back even the modest normalisation which has been laid down, thereby supporting risk assets in the near term.

A key concern for investors globally over the past few weeks has been the likely normalization of central banks’ easy money policies and the consequent impact on economies especially Emerging Markets (EM). Consequently, FPIs had been pulling money out from EM which in turn have continued to underperform Developed World equities through the year. Recent comments by Fed Chair however have acted to ease concerns a bit and FPIs appear to be looking at EM favorably again. Monetary policy in key developed markets may broadly stay accommodative considering the feedback loop into risk asset markets as well as to allow fiscal policy, the space to operate. We therefore expect normalization to be very gradual and well signalled. While the risks from policy mistakes are non-trivial, the bigger worry in the near term stays the course of the Virus and its impact on growth and inflation owing to continued, localized disruptions in several parts of the world.

Amidst these worries, Indian equities continued with their strong performance with the Nifty and the Sensex rising 8.7% and 9.4% respectively in August. On a relative basis, Indian equities have stayed strong outperformer relative to Emerging Market equities leading to a significant expansion in their valuation premium, with the latter having struggled on account of a combination of factors including Fed taper fears, renewed growth concerns and Chinese regulatory clampdown on Tech companies over the past few months.

Performance picture beyond large caps was not as rosy with the Nifty Midcap 150 gaining a more modest 2.1% and the Nifty Small Cap 250 declining 3% for the month. This was in sharp contrast to the trend of the past year or so wherein mid and small caps have significantly outperformed large caps. This reversal in relative performances was not completely surprising, however. We had highlighted last month that after the strong relative performance of mid-small caps versus large caps, their valuation differential had reverted to historical norms suggesting that the risk-reward was more balanced on that front now.

On overall equity valuations as well, the sharp run up has meant that even measures such as earnings yield relative to bond yields, attractiveness for equities has receded and a recovery in earnings is vital to support further upsides. And we continue to be constructive on corporate earnings. The strong prints on corporate earnings over the past few quarters at a time when economic growth is yet to find a footing suggests that the over a decade long declining trend on the corporate profits to GDP ratio has been arrested. At a time when economic growth has likely troughed, an uptick in profits to GDP could lead to non-linear uptick in earnings over the next few years. Thus, the longer outlook stays constructive premised on our view that we are in early stages of an earnings upcycle, even as investors would do well to moderate their return expectations. Key near term risk continues to be a stretched reading on our equity market sentiment measure, but we would continue advising any significant pullbacks to add on to pro-economy assets.

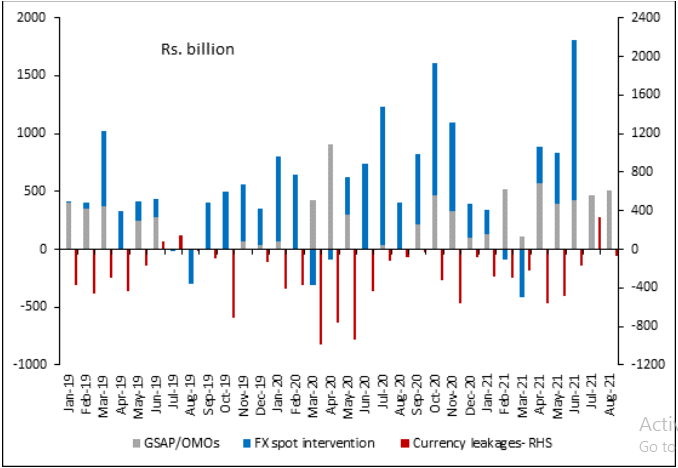

While the focus has remained on any tapering announcement by the US Fed, the RBI monetary policy has reaffirmed an accommodative stance, though with one MPC member’s dissenting opinion. The RBI did take hesitant steps towards normalisation of liquidity with the announcement of an increase in the 14 Day Variable Rate Reverse Repo auctions in stages to Rs 4 trillion from Rs 2 trillion. Subsequent interviews by the Governor have reaffirmed the dovish assessment as the RBI remains willing to tolerate Inflation closer to the upper end of the target range given the growth backdrop. While in the current environment, policy rate adjustments are ruled out, the tolerance for excessive liquidity, resulting in both the Weighted average Call rate as well as the Weighted average overnight rate trading much lower than the reverse repo rate has been supportive of market action in the recent weeks. This is evident from the chart below showing the monthly primary liquidity injection. CY21 y-t-d the net liquidity injected through Fx and Government bond purchases have amounted to more than Rs 5 trillion. Considering the impact of currency leakage, the net injection has been more than Rs 3 trillion which has led to systemliquidity surplus remaining closer to Rs 10 trillion.

The debate within the MPC as evident in the minutes, has been around modulating the excessive liquidity within the broader accommodative stance, even as Prof Verma dissentedaround the accommodative stance and preferred to raise the money market rates closer to the Repo rate.

Market action remains vulnerable to potential actions on liquidity in the near term. While the effective operating rate remains the reverse repo for monetary policy, the weighted average rate in the overnight markets remain way below the reverse repo and is likely to remain so in the near term. While the gradual increase in VRRR under the 14-day auctions may be a small shift, the efficacy of this to modulate either the quantum of liquidity or the price of overnight liquidity is doubtful. The asymmetric liquidity distribution within the system would have warranted market-based instruments such as Market stabilisation bonds/bills. The fiscal cost of a provision to conduct MSS T bill auctions to the extent of say Rs 4 trillion through 1 y bills would amount to less than Rs 150 Bn (at the latest cut offs in the auctions). The cost of a disorderly unwinding down the road would be felt through larger adjustments in borrowing costs across the system. Alternatively non- bank participants would need to be provided access to the VRRR auction being conducted, like the window provided by the US FED for Money market funds to access the central bank reverse repo facility.

While a delayed liquidity normalisation is a near term market positive, further delay in modulating the same even as flows remain robust would compound the problem of normalisation and lead to larger actions down the line with potentially destabilising impact on markets. The challenges faced by the RBI currently reflect the constraints of the “impossible trinity”. With an Open Capital account and Independent Monetary Policy, a fixed exchange rate cannot be sustained for long. By extension, Inflation Targeting, ultra-loose liquidity and targeting bond yields are conflicting objectives to the extent that all 3 cannot be simultaneously managed smoothly. Choosing loose liquidity and targeting yields through intervention may make inflation targeting difficult. With respect to the Trilemma of the Impossible Trinity, allowing currency appreciation as seen in recent times has been the trade off with intervention likely to worsen the problem of liquidity overhang. The potential impact that may have on exports, which have rebounded strongly in a positive global growth backdrop remains unknown. Interestingly export growth in April- Aug 21 has been around 23% higher as compared to the same period of 2019. Q1FY22 GDP data trends point to exports remaining the key support driver from the demand side even as Private Consumption andGross Fixed Capital formation lags on a 2y CAGR basis. Governmentspending remained muted relative to last year trends even as government revenues have shown a steady pick up in the fiscal year till date.

The current context provides a short-term window for tactical positioning with a slightly higher duration as the central bank signals have been dovish. Portfolio duration strategies need to be more flexible with downside protection. Consistent with an individual’s specific asset allocation framework, low to moderate duration exposure within the fixed income space may be ideal from a medium-term allocation perspective.